Crypto cards are surging, transforming stablecoins from digital holdings into practical instruments for everyday payments, according to a new report from analytics firm Artemis.

The sector, which connects digital assets to traditional payment networks, has grown from processing roughly $100 million per month in early 2023 to more than $1.5 billion monthly today, giving it an annualized market size of $18 billion.

The Artemis report, “Stablecoin Payments at Scale: How Crypto Cards are Eating the World,” shows that these cards leverage Visa and Mastercard infrastructure to enable seamless spending of stablecoins such as USDC and USDT.

Sponsored

Rather than replacing fiat systems, crypto cards act as an integration layer, allowing users to transact on-chain while maintaining global merchant acceptance.

Visa Dominates, Full-Stack Issuers Gain Ground

Visa accounts for over 90% of on-chain transaction volume among crypto cards, a lead driven by its early partnerships and established infrastructure. While both Visa and Mastercard support more than 130 programs, the market is increasingly shifting toward “full-stack” issuers like Rain and Reap.

These companies handle card issuance and settlement independently of sponsor banks, giving them greater control, higher margins, and less reliance on traditional financial intermediaries. Consumer-facing apps complete the ecosystem, allowing users to load and manage stablecoin balances with ease.

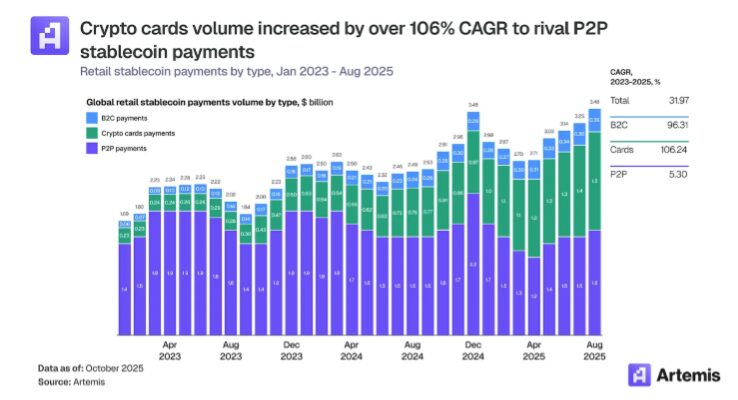

Artemis’s data, tracking retail stablecoin payments from January 2023 to August 2025, shows crypto cards soaring at a 106% compound annual growth rate (CAGR), reaching $106.24 billion in total. By comparison, peer-to-peer (P2P) transfers totaled $5.30 billion, while business-to-consumer (B2C) payments led the market at $96.31 billion.

Regional Trends Highlight Tailored Use Cases

Adoption differs across regions. In India, where crypto inflows hit $338 billion, crypto cards are mainly used for crypto-backed credit within systems like UPI.

In Argentina, they act as an inflation hedge, letting users convert volatile pesos into stablecoins for everyday spending.

In developed markets, the main draw is enabling high-net-worth users to spend large stablecoin balances smoothly, rather than filling gaps in existing payment systems.

Stablecoins as Global Bridge

Stablecoin adoption is expanding beyond early crypto users, with total supply over $308 billion and activity hitting all-time highs in December 2025.

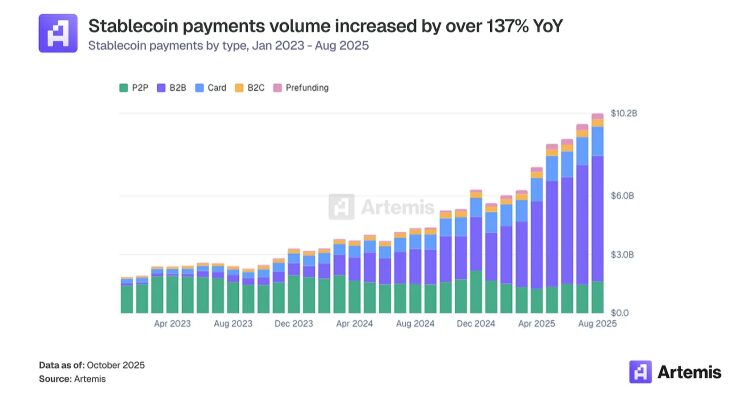

Stablecoin payments are entering a new phase of growth, with monthly volumes rising from $1.9 billion in January 2023 to $10.2 billion in August 2025. Growth is being driven by demand in emerging markets facing currency instability, improved user experiences, and rising institutional confidence in stablecoin payment networks.

Stablecoin cards have yet to match traditional credit offerings, but they appeal to financially engaged users with active on-chain activity and growing digital balances.

Looking ahead, Artemis expects crypto cards to continue expanding alongside stablecoin adoption, acting as a key bridge between digital assets and everyday commerce.

Although major networks such as Visa, Mastercard, PayPal, and Stripe are developing infrastructure for direct stablecoin acceptance, broad merchant adoption faces significant challenges like POS integration, regulatory compliance, and consumer trust, making a full transition a multi-year, potentially decade-long process.

Why This Matters

Crypto cards are turning digital assets into usable money, giving stablecoin holders real-world spending power and signaling the growing integration of crypto into mainstream finance.

Check out Ciphera’s trending crypto news today:

Dogecoin’s “Third Test” Zone Loaded, Price Presses Key-Range High

Coinbase Withdraws Backing, Senate Crypto Bill Stalls

People Also Ask:

Crypto cards allow users to spend cryptocurrencies or stablecoins like USDC and USDT at merchants that accept Visa or Mastercard, converting digital assets into fiat at the point of sale.

Crypto card transactions use traditional payment networks’ security protocols and compliance standards, including fraud protection and KYC/AML oversight, though users should still exercise caution with digital assets.

Not yet. While they offer spending convenience, crypto cards currently lack full credit features like unsecured credit, extensive rewards programs, and global merchant acceptance compared with traditional cards.